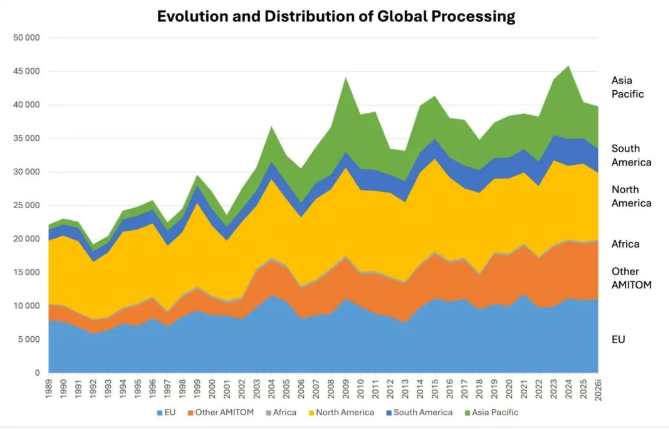

Negotiations on 2026 production volumes and prices are still ongoing in the Northern Hemisphere, while harvesting in the Southern Hemisphere is nearing completion. According to the latest estimates from the World Processing Tomato Council (WPTC), global processing tomato production is expected to be below 40 million metric tons, currently estimated at 39.8 million metric tons. This represents a slight decrease from the final 2025 output of 40.3 million metric tons, and is considerably lower than the surplus volumes recorded in 2023 (44.4 million metric tons) and 2024 (45.9 million metric tons).

AMITOM Member Countries

Bulgaria

Due to rising energy and fertilizer costs (+40%) and planned renovations at the largest facility, Balkan, 2026 processing volume is expected to drop by 50% to 20,000 metric tons. Current weather is slightly wet but will not impact sowing scheduled to start at the end of April.

Egypt

Forecast remains unchanged at 800,000 metric tons.

France

Uncertainty persists as price and production negotiations are ongoing. Production is expected to decrease to 150,000 metric tons, likely accompanied by a reduction in conventional acreage, while organic acreage is projected to increase. Total planted area will be less than 2,000 hectares.

Persistent winter rainfall has left fields wet and conditions unfavorable. Transplanting, originally scheduled to start this week, may be delayed until next week due to current windy and cold weather.

Greece

Weather is favorable and fields are prepared. Planting began this week in the southern regions and will start next week in central areas. The main concern is the impact of the war on energy and fertilizer prices, despite some government support. Forecast remains at 450,000 metric tons.

Prices have been announced, averaging approximately €115/mt (delivered to factory), with some variations.

Hungary

Current forecast is around 70,000 metric tons. Nursery seeding started last week.

Iran

High uncertainty remains, and communication is difficult. Iran has temporarily banned exports of tomatoes and tomato products. Further updates will be provided as information becomes available.

Italy

Overall water availability in northern Italy is sufficient (wet winter), and soil preparation is in good condition. The forecast remains at the level published in February (3 million metric tons).

Negotiations between processors and grower associations over production volumes and economic conditions faced a series of delays and difficulties due to volatile energy costs, which impact not only fuel for agricultural operations but also input costs including nitrogen fertilizers. Negotiations finally concluded on Friday, March 27, with an average field delivery reference price of €137/mt, including late-delivery premiums and service fees.

Conditions in central and southern Italy are better than last year, with adequate water supplies in many areas. However, the Occhito Dam, while improved, still does not fully resolve water shortages.

As usual, processors and grower associations in central/southern regions will wait for northern prices to be finalized before beginning their own negotiations.

International tensions related to the Strait of Hormuz have raised significant concerns over diesel and fertilizer costs, creating headwinds for negotiations.

The forecast has been revised to 2.8 million metric tons for central/southern Italy, bringing the national total expected production to 5.8 million metric tons.

Portugal

Portugal has been affected by multiple storms, with widespread flooding in tomato-growing areas. Some field boundaries along the Tagus River have been damaged, leading to waterlogged land. Current favorable spring weather is helping dry remaining flooded areas. Transplanting is scheduled to begin on April 6.

The estimate of 1.3 million metric tons is therefore maintained. Seasonal prices are reported in media at approximately €106–107/mt (field delivery).

Serbia

Conditions to date are favorable. If yields reach last season’s level of approximately 90 metric tons per hectare, processing volume is expected to be 57,000 metric tons.

Spain

Ample winter rainfall has filled reservoirs in Andalusia and Extremadura, ensuring good water supplies for the next four years. Weather is currently favorable; planting began last week in Andalusia and will start next week in Extremadura.

Prices have been agreed at approximately €107/mt (field delivery) or €115/mt (delivered to factory). However, some farmers are now requesting higher prices due to rising energy and fertilizer costs. Forecast raised to 2.75 million metric tons.

Tunisia

No processing forecast for the season is yet available. The only available data is the planned planted area, estimated at approximately 15,300 hectares.

Turkey

Based on collected information, planted area may decrease slightly in the south while remaining stable or increasing marginally in the Bursa region. Weather was wet last week and more rain is expected next week, so planting will be slightly later than usual.

Product stocks (mainly canned tomato paste) remain, and exports have declined due to unfavorable exchange rates. Production is expected between 2.4 and 2.5 million metric tons.

No public price data is available, but contract prices are around TRY 525/mt (delivered to factory), equivalent to €100. Farmers are demanding higher prices due to increased costs; otherwise, they may reduce fertilizer use, which would impact yields.

Ukraine

Fields are prepared, nursery seeding has started on schedule, and transplanting is planned for late April. Fertilizer supplies are sufficient but prices are considered unreasonable, and energy prices have also risen. The forecast may be revised downward in May based on actual field conditions. Frontline positions remain unchanged from one year ago.

Other Northern Hemisphere Countries

California

Planting of early-season crops began in February under ideal weather conditions. March has brought above-normal temperatures, favoring plant growth in already-planted fields. Warmer temperatures also caused brief pauses in some planting activities, but no major issues are expected at this time.

Rainfall received this year is below earlier winter expectations, which will reduce water allocations in some parts of the state. Since planted area has already contracted this season, reduced water allocations will not affect actual planted area for the current campaign.

Price negotiations are still ongoing.

Canada

Initial contract intentions for 2026 are 586,000 short tons (approximately 532,000 metric tons). Typical early spring weather has prevailed over the past few weeks, including alternating warm and cold periods, cloudy skies, intermittent rain, occasional wet snow, and several nights with sub-freezing temperatures. Planting is scheduled to begin in early to mid-May.

China

As of the end of March, the planted area for processing tomatoes is approximately 50,670 hectares. Production is estimated at 5.92 million metric tons. The downward revision is mainly due to cautious farmer sentiment toward market outlook and lower planting enthusiasm.

Japan

Planting will begin in phases starting at the end of March, beginning with the Tokai region. Forecast unchanged: 400 hectares planted, processing volume expected at 24,000 metric tons.

Southern Hemisphere Countries

Argentina

The 2026 processing tomato campaign in Argentina has harvested approximately 75% of planted area, entering its 13th week of harvesting. Planted area is estimated at 5,120 hectares. Under normal yield conditions (in line with the multi-year average), total production is expected to reach approximately 425,000 metric tons.

Yield expectations remain strong and stable, supported by strong performance under the Tomate 2000 program, which has effectively mitigated the impact of recent hailstorms. Current yields are 10–15% above last season, showing continued improvement over 2025. Overall crop condition is good, and fruit quality has been highly satisfactory to date.

Weather conditions this season have been generally stable: warm, dry, windy, and with limited rainfall. However, a severe hailstorm hit the Villa Aberastain area of San Juan Province in mid-January, affecting an unusually large area of approximately 400 hectares, with damage ranging from minor to severe.

Harvesting began in mid-December and has progressed steadily. While accelerating around Weeks 5 and 8, it has since returned to a normal pace. Harvesting is on track and expected to conclude in late April, depending on factory scheduling and remaining field conditions.

Within the Tomate 2000 program, which accounts for a large share of national production, progress is slightly ahead: 76% of adjusted area has been harvested (2,160 hectares out of 2,842 total hectares). The program’s total expected production is approximately 293,228 metric tons, of which 229,535 metric tons have been harvested, leaving about 63,700 metric tons remaining.

Average yield from harvested fields is currently estimated at 106 metric tons per hectare, confirming strong production performance this season.

The Tomate 2000 program’s share of national output continues to rise, now representing approximately 68–69% of total expected production. This growth is mainly driven by excellent results in supervised areas, where yields are higher and more stable, consistently above the national average. The program thus plays an increasingly central role in supporting Argentina’s overall production level.

Clear regional differences exist within the program.

In the San Juan region, an early-maturing area, crop progress is significantly advanced: 86% of area harvested, with only 14% remaining. Harvested yields are strong, averaging around 111 metric tons per hectare, confirming robust performance.

In contrast, the Mendoza region, a later-maturing area with cooler climates, has harvested 54% of area, with 46% remaining, representing most of the outstanding harvest. Despite slower development, harvested yields are also strong at approximately 91 metric tons per hectare, showing stable performance under less favorable heat conditions.

Australia

National harvesting is nearly complete but has slowed due to widespread rainfall. Cumulative deliveries to date are approximately 138,000 metric tons, with total production expected to reach around 157,000 metric tons, down from earlier forecasts. Processing is expected to end shortly after Easter.

Brazil

Current forecast is 1,467,000 metric tons from 15,150 hectares.

According to a 2025 Rabobank study, tensions in Iran could impact the fertilizer market, particularly nitrogen fertilizers. The study notes that approximately 45% of global urea exports, 25% of ammonia, 20% of DAP, 10% of MAP, and nearly 30% of sulfur are shipped via routes associated with the Persian Gulf. Agricultural diesel prices have already risen by 60% in one week.

Chile

Heavy rainfall affected various tomato-producing regions around mid-March, with some areas recording over 100 mm in 24 hours on March 16. All factories operated last week but at lower throughput. A full assessment of rainfall damage is not yet possible, so the forecast remains at 1.3 million metric tons.

New Zealand

Processing tomato volume has decreased this year due to high existing inventories of tomato paste held by the only remaining processor, Heinz Watties. Focus has shifted to canned products, so the factory will process only 15,000 metric tons, down from 37,000 metric tons in 2025.

South Africa

Summer production areas are experiencing dry, hot weather. Seventy-five percent of summer crop deliveries have been received, with an average Brix of 5.8. The summer processing season is expected to end in late April. Timely deliveries currently represent 25% of total South African processing volume.

In the northern Limpopo province’s winter production areas, flooding has been reported. Transplanting should be completed by the end of April. Winter deliveries are scheduled from April through late September.

Post time: Apr-03-2026